Land News

Why August Is the Perfect Time to Prepare Land for Fall Hunting Season

August is the perfect time to prepare your land for fall hunting. Discover essential tips to improve habitat, access, and overall property readiness.

Published date:

Last updated date:

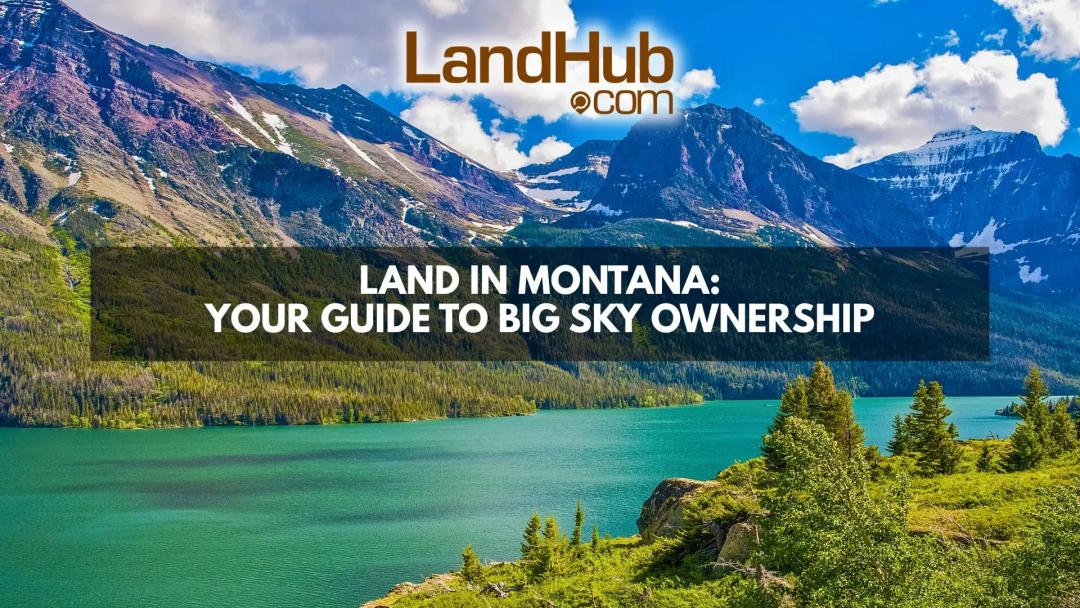

Land in Montana: Your Guide to Big Sky Ownership

Discover everything you need to know about buying land in Montana, from top regions and property types to ownership tips, investment opportunities, and the benefits of Big Sky living.

Published date:

Last updated date:

Why July Is One of the Best Months to Buy Rural Land

Discover why July is one of the best months to buy rural land, with seasonal opportunities, motivated sellers, and ideal conditions for property tours.

Published date:

Last updated date:

HOA Restrictions on Land: Here’s What to Know

Learn how HOA restrictions can affect land ownership, property use, building plans, and what to review before buying land in an HOA community.

Published date:

Last updated date:

Building Generational Wealth Through Land Ownership

Learn how land ownership can help build generational wealth through long-term appreciation, income opportunities, and a lasting family legacy.

Published date:

Last updated date:

20.webp&w=1080&q=75)

Development Trends That Impact Local Land Values: What Buyers and Sellers Need t

Explore the key development trends shaping local land values and learn what buyers and sellers should know before making their next move.

Published date:

Last updated date:

Land for Sale in the USA by State

- Alabama

- Alaska

- Arizona

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montana

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Puerto Rico

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Vermont

- Virginia

- Washington

- West Virginia

- Wisconsin

- Wyoming